QUICK QUOTE

Complaints Handling Policy

COMPLAINTS HANDLING POLICY

1.1 Purpose

2XL Commercial Finance Ltd (the Firm) has implemented a Complaints Handing Policy to

ensure that it is able to handle customer complaints quickly, easily and in a transparent

manner. Complaints must also be handled fairly and provide consistent outcomes for all

customers, as required under the FCA’s Principle of Treating Customer Fairly.

1.2 Definition of a complaint

A complaint is defined as any oral or written expression of dissatisfaction, whether justified

or not, from, or on behalf of, a person about the provision of, or failure to provide, a financial

service or a redress determination, which:

(a) alleges that the complainant has suffered (or may suffer) financial loss, material distress or

material inconvenience; and

(b) relates to an activity with the Firm has provided in relation to the provision of portfolio

management, financial services or marketing of products.

Other matters raised to the Firm, which do not fall under of the definition of complaint may

not be treated as a complaint. However, in the interests of treating all customer fairly, some or

all of the following procedures may still be adhered to and the company will deal with all its

customers in an open and honest manner.

1.3 Definition of an Eligible Complainant

An eligible complainant is defined in DISP 2.7.3R and include the following:

a) A consumer (any natural person acting for purposes outside his trade, business or

profession);

b) A micro enterprise (a person carrying on an economic activity who employers fewer

than 10 person and has a turnover or annual balance sheet of less than €2 million);

c) A charity which has an annual income of less than £6.5 million; or

d) A trustee of a trust which has a net asset value of less than £5 million.

In addition to meeting the criteria above the eligible complainant must have a complaint which

arises from their relationship with the firm as outlined in DISP2.7.6R. This includes:

a) The complainant is or was a customer or potential customer of the Firm; and the

complaint has arisen from matters relevant to their being or having been a customer.

b) The complainant is the holder or beneficial owner of units or shares in an AIF for

which we are the AIFM.

Eligible complainants may refer their relevant complaint to the Financial Ombudsman Service (“FOS”)

should they be dissatisfied with the firm’s response.

The Financial Ombudsman Service can be contacted at: www.financial-ombudsman.org.uk

or Exchange Tower, London E14 9SR. Tel: 0800 023 4567 or 0300 123 9 123

It is expected that not all of our clients will be eligible complainants.

1.4 Scope of the policy

The Policy applies to all individuals working within the Firm and will govern all complaints

made by customers. All complaints should be immediately directed to The Director.

1.5 Information on our complaints policy

We have prepared a summary of our complaints policy and we will provide this summary to

eligible complainants free of charge if requested, and at all times when acknowledging an

complaint.

1.6 Procedure

(i) Procedure for complaints from clients which are not eligible complainants

If a complainant is received from a party which is not an eligible complainant the rules on

complaints handling do not apply. However, we will follow the process below:

1. Any complaint received, whether verbally or in writing, must be notified to the

Director.

2. The Director will investigate the facts surrounding the complaint and attempt to

resolve it without delay.

3. The Director will liaise with the Compliance Officer who will maintain a file of all

complaints received and subsequent correspondence.

(ii) Procedure for complaints from clients which are Eligible Complainants

The following complaints procedure should be followed if a complaint is received from an

eligible complainant in accordance with Dispute Resolution:Complaints Handbook (DISP) 1.

1. If a formal complaint is received it should be referred to the Director and the

Compliance Officer immediately.

2. Where the complaint has been made verbally the client, we will email the complainant

asking for confirmation of the nature of the complaint so that a record is held in writing

for both parties. However, it should be noted that failure to provide or acknowledge a

complaint in writing by the client does not remove the Firm’s obligation to investigate

the complaint and treat the customer fairly.

3. Complaints should be resolved as soon as possible. The Firm has three business days

(after having received the complaint) in which to resolve the complaint. The Firm will

not be required to send the complainant a final response letter if the complaint has

been resolved within this timeframe. However, the Firm is required to send the

complainant a summary resolution communication which will contain details of how

they can direct their complaint to the FOS, should they be dissatisfied with the

resolution provided by the Firm. The complaint will be considered closed when the

client has accepted the summary resolution by the client or if no response has been

received within 2 weeks, following the provision of the summary resolution.

4. Where it has not been possible to resolve a complaint within three business days the

Director and the Compliance Officer will take responsibility for ensuring its

resolution.

5. Where a complaint cannot be resolved within three business days, the Firm has an

obligation to promptly acknowledge the complaint and provide the complainant with

a copy (or summary) of its complaint handling procedures.

6. The Firm then has an ongoing obligation to keep the complainant informed of the

progress of his complaint (DISP1.6).

7. The Firm must, within eight weeks after its receipt of a complaint, send the

complainant:

• A final response; or

• A written response, which:

– Explains why it is not in a position to make a final response and indicates

when it expects to issue one;

– Informs the complainant that she/he may refer the matter to the FOS; and

– Encloses a copy of the FOS explanatory leaflet.

A complaint is closed where the Firm has sent a final response, or the complainant has indicated

in writing its acceptance of the Firm’s earlier response.

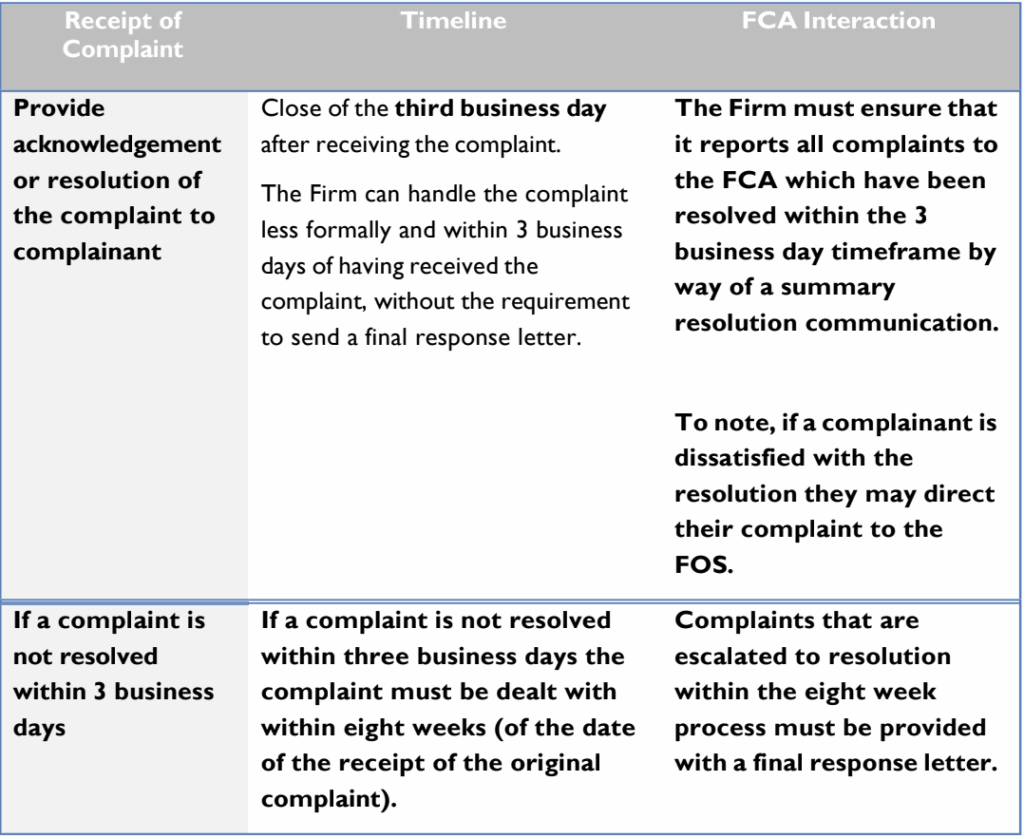

1.7 Complaints handling timeline

If a complaint is received, the following timeline must be adhered to:

To note, we understand that the definition of the close of the business day relates to the

ordinary business hours in which the Firm operates. To confirm these business hours are:

• 9:00am – 5:00pm Monday to Friday.

The Firm will ensure that it has the appropriate staff in place to receive complaints and

that staff will engagement at the appropriate points in the handling of each complaint.

The Firm will evidence the approach taken by the Firm in handling the complaint, particularly

in relation to the conclusion of each complaint.

1.8 Summary resolution communication

Where the Firm is able to resolve a complaint within three business days we will provide

the complainant with a summary resolution communication to ensure that they are

aware of all the avenues of recourse open to them in raising a complaint. The summary

resolution communication will inform the complainant of their right to refer their

complaint to the FOS, if they are dissatisfied with the decision made by 2XL Commercial

Finance Ltd.

In certain cases, even though we have resolved the complaint, we may suggest that the

complainant refers their complaint back to us in order for us to review it further. In

these cases we will ensure that the complaint has been fully resolved within eight weeks

of the original receipt of the complaint.

If a complaint is resolved verbally, we will inform the complainant that the resolution will be

provided in writing, i.e. in the form of a written summary resolution communication.

1.9 Record keeping

For each complaint received these will be maintained on file. All complaint records will

be kept on file for five years from the date of the complaint.

1.10 Reporting to the FCA

Twice a year the Firm will complete the FCA’s complaints return via the RegData system.

The Firm will disclose all complaints, including those resolved within three business

days. Where we have received no complaints, we will provide the FCA with a nil return.

1.11 Contact Details

Contact details of the Complaints Function:

The Director

2XL Commercial Finance Ltd

darren@2xlcommercial.com